What the Watch Industry Cannot Admit

The Luxury Watch Demand Problem Nobody Wants to Name

Long time industry commentator Ariel Adams recently wrote about industry pricing and survival: that there is a diagnosis the luxury watch industry has quietly settled on. It goes something like this:

The customers who used to buy our watches have been priced out.

The middle class has hollowed out.

Discretionary income is under pressure.

Geopolitical uncertainty is making everyone cautious.

It is a difficult environment, and we are managing through it as best we can.

This is not false, but it is incomplete, and that is doing damage because it shelters the industry from a more uncomfortable question:

What if too many buyers simply no longer feel the urgency to spend on a watch?

The Comfortable Diagnosis

Macroeconomic explanations have genuine merit. The wealth distribution data, the erosion of the upwardly mobile middle-class buyer and the shift away from aspirational, impulse purchasing toward more deliberate, research-driven acquisition is real. None of that is invented.

But macroeconomics has become a shelter. When you attribute flat or falling sales to economic headwinds, you are describing a problem that is external, structural, and largely beyond your control. You wait for the cycle to turn, manage costs and survive. Nobody’s strategic judgement is implicated nor product decisions questioned. Nobody has to ask whether the product has become less compelling than its price.

The alternative explanation is far harder to sit with: that demand may be weakening because watches have become, for a growing number of potential buyers, less necessary, less culturally alive, and less emotionally important than they once were.

That is not a macroeconomic problem, it’s a product and culture problem. And it requires a completely different response.

I examined how that product and culture problem develops inside individual brands in an earlier piece. What follows is about what happens when it develops across an entire industry.

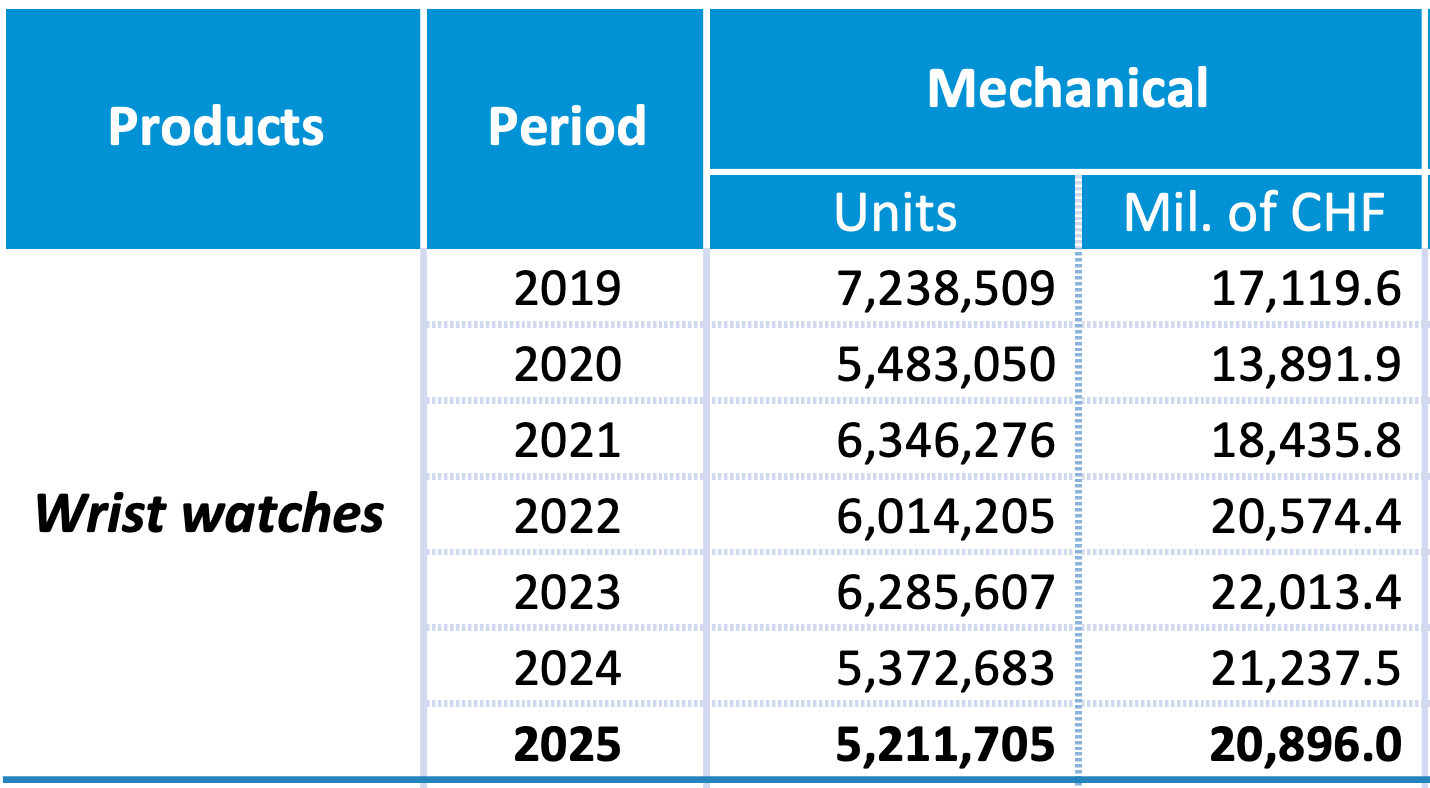

Source: FHS.swiss

Three Problems, Not Two

It is tempting to frame this as a simple binary: either customers cannot afford watches, or they can afford them but don’t want them but, the more precise diagnosis is a third thing.

Customers may still want watches. Just not these watches, at these prices, through this retail experience, under these allocation games, with this thin a cultural argument.

That is a more specific and more actionable indictment. It does not say the category is dying, but that the industry has been making it progressively harder to justify the purchase, and has been confusing the resulting hesitation with an affordability problem.

Hesitation and inability are not the same thing. The response to inability may be a lower price. The response to hesitation is a better product. Much of the industry has been trying neither. We covered the failure mechanisms and what to do about them here.

What the Secondary Market Is Telling You

Secondary market pricing is not a perfect measure of desire. It is contaminated by speculation, leverage, dealer inventory, currency movements, grey-market overhang, and brand-specific hype cycles. But, it is a useful lie detector.

The broad secondary-market indices have been telling this story for some time. With listings of dozens of references available below retail. That does not prove the whole market has lost desire. It does show that scarcity language and market-clearing reality have parted company. The brand believes the watch deserves a certain price. The market, populated by real buyers spending real money, disagrees.

And critically, this is not about buyers being priced out. It is about buyers being unconvinced. Not enough of them ‘want in’ at the prices the brands still believe their watches deserve. That gap, between what a brand thinks its product is worth and what a buyer will actually pay, is the real metric. And for a wide range of established, current-production references, that gap has been widening for several years.

Why the Industry Cannot Admit This

The institutional resistance to the desirability diagnosis is entirely rational, if you understand the incentive structure.

Admitting that customers have lost interest requires answering genuinely difficult questions. Is the product still relevant? Is the cultural status it confers still valued, by the people you most need to value it? Is the storytelling still compelling in an era when buyers arrive already more informed than your marketing team? Is the price defensible against every alternative competing for the same budget and emotional space?

Blaming macroeconomics requires none of that. You simply wait for the world to improve.

The danger is that waiting is exactly the wrong response to a desirability problem. Categories that lose cultural urgency do not recover through patience. They recover through reinvention, or they calcify, becoming progressively more expensive, more niche, and more dependent on the same collectors, the same anniversaries, the same archive references, and the same inherited claims to importance.

At that point, the affordability problem the industry has been citing becomes a self-fulfilling prophecy: not because buyers could never afford the watches, but because not enough of them ever decided they needed to.

Where the Money Actually Is Going

Wealthy consumers have not stopped spending. This is important, because it closes off the affordability excuse entirely at the top of the market. The people who can afford serious watches are still making serious purchases. They are spending on experiences, on cars, on property, on art, on things that feel culturally alive and personally meaningful.

The question worth asking is why those categories are capturing discretionary budget that watches are not.

This is visible in the swollen middle market and product calendar of almost any major brand: a steady procession of coloured dials, archive references, and ‘icons’ that seem to have been declared rather than earned. The issue is not that these watches are necessarily bad. Many are competent and some are excellent, but the problem is that competence at a higher price is not the same as desire.

The categories still capturing money tend to deliver one or more of the following: lived utility, genuine social currency, active cultural participation, or a visible transformation of how you experience your life. A great car changes how you move through the world every day. A significant piece of art anchors a room and a conversation for decades. An exceptional experience is unrepeatable and therefore precious.

Too many watches, particularly in the mid-to-upper price ranges where the industry has been most aggressively repricing, now struggle to make that case. The problem is not that a 20,000CHF watch is expensive. The problem is that too many 20,000CHF watches cannot clearly explain why they matter beyond the fact that the brand says they do.

Heritage and artisanship are real, but neither of those things, repeated loudly enough on a product page, constitutes an emotional reason to buy. They constitute a justification, which is what you reach for when desire is weak.

The Solution Is Not Discounting

I want to be clear about what I am not arguing. This is not a case for lower prices or for making luxury watches more democratic. Accessible pricing does not fix a desire problem. A watch that nobody urgently wants at 15,000 is not automatically more compelling at 10,000. You have just made the margin problem worse.

The solution is rebuilding genuine reasons to care. That starts with product decisions, not pricing theatre. It means fewer hollow launches, fewer inherited claims to importance, better aftersales, more credible technical substance, and stronger reasons for a buyer to feel that this watch belongs in their life rather than merely in the brand’s catalogue.

The industry knows how to do this; it has done it before. The question is whether it can first acknowledge that the problem it is facing is one of desire, not just demographics, and that the comforting story it has been telling itself is holding it back from the harder, more honest work of solving it.

The industry does not merely need demand to recover. It needs to become more worth desiring.

The Price Increase That Mistook Wealth for Desire

The watch industry correctly identified one important thing: the future buyer was going to be wealthier.

That much was true. The mass aspirational customer was becoming harder to reach. The old middle-class upgrade path was weakening. The department-store version of luxury had lost much of its magic. Younger buyers were less loyal to inherited status codes, more sceptical of traditional prestige, and more willing to spend serious money elsewhere. If watches were going to keep growing, brands would need to move closer to the affluent customer, the global collector, the HNW buyer, the person for whom a five-figure purchase was uncomfortable perhaps, but not impossible.

So far, so rational. Then the industry made the classic luxury-sector mistake. It confused the existence of wealth with the existence of desire.

It looked at the top of the market, saw that some customers could pay more, and concluded that many watches should cost more. Prices rose, product ladders were repositioned, entry points became less entry-like. Icons were repriced as crown jewels, ordinary references were dressed in the language of allocation, scarcity, and privilege. The result was not elevation. In too many cases, it was simply inflation.

The strategic insight was sound, the execution much less so.

Wealth Is Not Permission

There is a dangerous sentence that sits quietly behind much of the industry’s recent pricing behaviour: the customer can afford it.

Perhaps they can. That does not mean they should. More importantly, it does not mean they will.

Luxury pricing only works when the buyer accepts not merely the product, but the logic of the product. A high price is not, by itself, a problem.

In luxury, price is part of the architecture. It creates distance, signals seriousness, protects margin, slows demand, reinforces status, and tells the buyer that what they are entering is not ordinary commerce.

But price only performs that function when it is supported by conviction. The buyer has to feel that the watch has earned its place: through design, movement, finishing, rarity and cultural force. Through a coherent place in the history of the brand. Through a sense that, even if the price is uncomfortable, it is not arbitrary.

That is the line many brands have crossed.

They have not always made their watches meaningfully better, simply more expensive. Then they have mistaken the absence of immediate collapse for proof that the market agreed.

It didn’t, it’s just slow to object.

The Hollowing Out of the Middle

The true summit has its own strange physics. There, scarcity can be real, craft can be extreme, patronage still matters, and the buyer is often seeking something beyond conventional value.

Nor is the greatest pressure necessarily at the bottom, where strong design, honest pricing, and direct-to-consumer energy can still create momentum.

The most exposed part of the market, the danger zone, is the swollen middle: watches expensive enough to require justification, but not special enough to supply it.

This is the CHF 5,000 to CHF 20,000 band, broadly speaking, though the exact limits vary by brand, market, and category. It is where the industry has tried to move huge volumes of product upmarket while keeping too much of the underlying proposition familiar. Steel sports watches. Integrated bracelets. Archive divers. Chronographs with inherited names. Dress watches with borrowed seriousness. Limited editions without real limitation. Manufacture movements whose main achievement is that they are not from someone else.

Some of these watches are good. A few are excellent. But the buyer is no longer being asked to pay for good. They are being asked to pay for significance and that is a much harder sale.

The Manufacture Movement Trap

No phrase has been more useful to modern watch pricing than “in-house movement.” It allowed brands to imply vertical seriousness, technical legitimacy, and collector-grade substance in three words. For a while, it worked. The market had been trained to treat dependency as weakness and autonomy as virtue.

The problem is that “in-house” became a label. A genuinely excellent proprietary movement can absolutely justify price. The movement is not a decorative credential. It is the engine of the watch, and in a serious watch it should be treated with seriousness.

Architecture. Thinness. Efficiency. Finishing. Durability. Precision. Anti-magnetism Winding performance. Serviceability. They all matter. But too many manufacture movements became pricing instruments. They were used to justify elevation without being asked to carry enough technical burden. The power reserve increased, perhaps. The bridge shape changed. The rotor acquired a logo. The press release said “developed exclusively.” The price moved north.

Buyers are not stupid. They may not understand every detail of escapement geometry or barrel torque, but they can sense when a claim has become ceremonial. They know when “manufacture” is being used as a substitute for excellence rather than evidence of it.

That worked in a market drunk on validation. It works less well in a market asking harder questions.

Scarcity Became Theatre

The other great pricing support was scarcity.

Real scarcity is powerful. It requires discipline, lost sales, slower growth, difficult allocation choices, and a willingness not to feed every market that waves a purchase order. Proper scarcity is not a slogan, it is a cost structure.

Much of what the industry called scarcity was something else: controlled release, boutique friction, allocation games, and artificial opacity. The pleasant little humiliation of being told that a watch was not available, followed by the discovery that everyone else somehow seemed to have one.

That kind of scarcity works only while buyers believe in the game. Once they stop believing, the same mechanisms that created heat begin to look like contempt. The waiting list becomes theatre. The boutique relationship becomes managed dependency. The collector journey becomes a sales funnel wearing gloves.

This is dangerous because luxury relies on voluntary submission. The buyer accepts inconvenience, opacity, and hierarchy only when they believe the object and the institution deserve it. If the belief goes, the ritual curdles quickly.

Nobody wants to be patronised by a shop that cannot clear its own stock.

The Rich Are Not a Segment

Another mistake was treating “wealthy buyers” as if they were a single category.

They are not. The serious collector, the status buyer, the design-led client, the engineering obsessive, the patrimonial buyer, the speculator, the newcomer, the family-office client, the enthusiast with one major purchase left in them, and the bored rich client looking for novelty do not buy the same thing for the same reason.

A higher price may attract one and repel another. It may increase status for one buyer and destroy credibility for another. It may make a watch feel more serious to a client who wants distance, and more ridiculous to a client who knows too much.

This is where the industry’s new faith in high-net-worth demand becomes crude. Wealth does not erase discrimination. Often it increases it. The buyer who can afford anything is not liberated from choice, they are burdened by it. Every object has to compete not only with its category rivals, but with the buyer’s sense of taste, identity, time, opportunity cost, and embarrassment.

That last word matters.

Luxury does not merely have to be expensive. It has to avoid making the buyer feel foolish.

The Embarrassment Threshold

There is a point at which a watch becomes difficult to defend even to oneself.

Not because the buyer cannot afford it. Not because the watch is bad. Not because luxury needs a utilitarian justification. But because the gap between price and meaning has become too visible.

The issue is not a single brand. It is the 7,000 CHF diver that used to be a 4,000 CHF diver, the 15,000 CHF integrated bracelet watch that wants to sit near icons without having become one, and the 18,000 CHF chronograph whose movement story is less interesting than its invoice.

This is why the last seven year’s repricing is so dangerous. It moved many watches into bands where the old arguments no longer suffice. The same movement, the same bracelet, the same dial logic, the same design family, the same service experience, and the same marketing vocabulary now have to survive a much harsher level of scrutiny. Many of these watches were persuasive as upgrades. They are weaker as ‘ultimates’.

What Actually Justifies a Higher Price

A higher price can be justified, this article is not anti-price, it is anti-unearned price.

There is a simple test for this, and many recent price increases would struggle to pass it.